“If I was a media planner and you gave me the first dollar, would I spend it in retail media? The answer would be no. But if we don’t invest, we might not be findable — and if we’re not findable, it’s the equivalent of not being distributed at a retailer.”

That quote says it all.

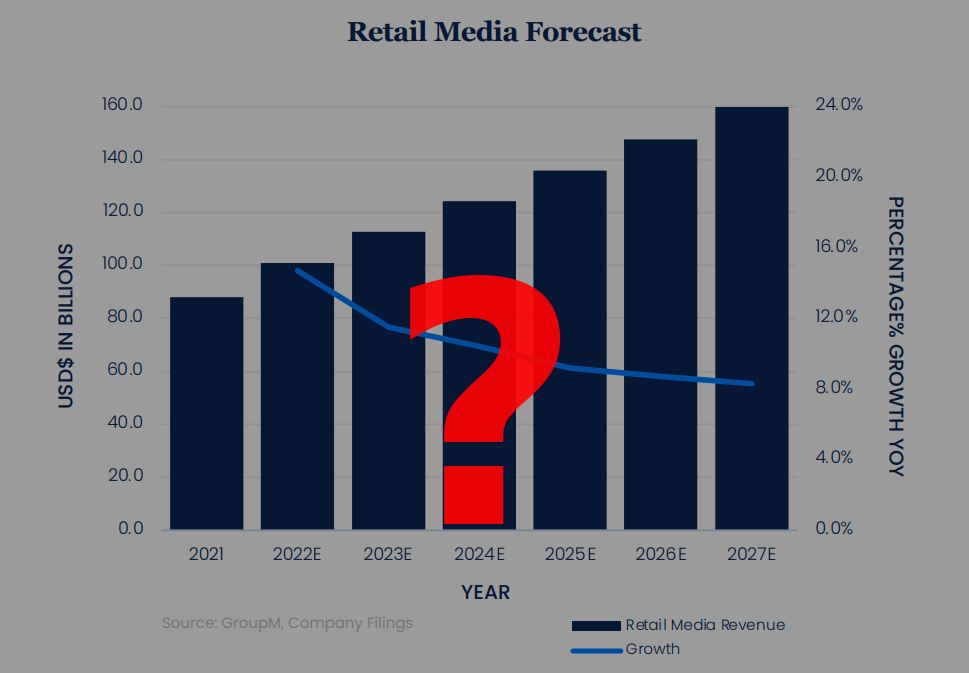

The first wave of retail media growth is over.

The hype phase — the one driven by platform launches, inflated expectations, and “just add budget” momentum — has peaked.

Now comes the hard part: maturity.

Up to now, it’s been “grow, baby, grow” — more retailers, more platforms, more inventory, more spend. Retail media’s YOY growth figures have been eye-watering.

But in 2025?

With economic uncertainty, tighter budgets, and pressure on every dollar, there’s a shift happening. A sharper, more sceptical lens is being applied — not just by brands, but by media planners.

A recent ADWEEK piece (link in comments) is one of the first trade articles to go overtly negative on retail media.

It raises some uncomfortable but important questions:

• Is retail media actually valuable on a media plan?

• Are joint business plans just a lever for forced spend?

These topics reflect some of the core critiques of retail media investment:

❌ “It’s not advertising, it’s a distribution tax that creates more margin for retailers.”

❌ “It doesn’t drive incremental sales — it just harvests what would’ve happened anyway.”

Of course, the reality is more nuanced. It’s contextual. It depends on category, retailer, audience, and execution.

But here’s the shift:

We’re entering a more transactional, negotiation-heavy era between brands and retail media owners. Less blind growth. More scrutiny.

That’s a good thing.