It’s probably not controversial anymore to say we are accelerating into the biggest disruption in travel distribution of all time. Three years ago today, nobody talked about any kind of upcoming threat to the dominance of Google. In a year from now, Google may be unrecognizable from the default UX today, and there’s a good chance that a majority of travel websites might have experienced 30%, 50%, maybe higher declines in website traffic.

So in this future of AI search and discovery, and of AI agents, who will emerge as the winners and the losers.

Some assumptions:

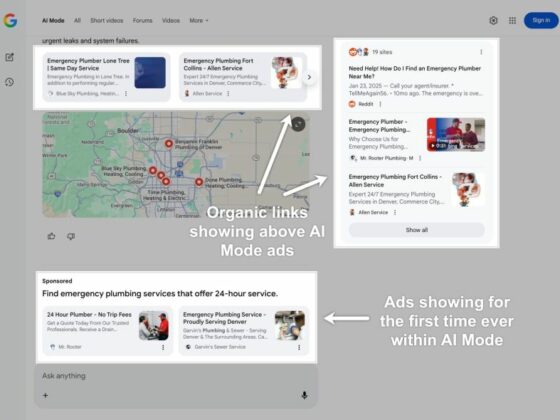

- Search will end up with a UX somewhere in the ballpark of Google’s AI mode today.

- The foundation LLMs will be the starting point for most search & discovery: Google, ChatGPT, possibly Meta and maybe Apple if they wake up. One or more of these models will be your primary personal agent.

- Traffic will mostly stay on-platform. Traffic to websites will still happen, but most information will transfer within the chatbot platform, and increasingly transactions will also happen within the LLM interface from end-to-end.

One way to think about this is as a shift from a “pull” model (user pulls info from links) to a “push” model (AI pushes a generated & curated solution)

Let’s look at how that shakes out for a few of the interested groups.

1. Intermediaries & OTAs

Existential threat to their role as the primary customer interface.

The marketplace or the platform had so many fundamental advantages over what preceded them. Much like Google, this wasn’t a conversation that was happening at all 3 years ago. But LLMs run right over the core advantages of the platform model.

- Disintermediation: The AI becomes the new aggregator. A user asking, “Find me the best hotel in Paris for my anniversary,” will primarily get an answer from the AI, not a link to an OTA. The OTA’s direct relationship with the customer is intercepted.

- Who offers the value: OTAs were untouchable because of their economies of scale and network effects. Those things don’t matter in this new world. The AI has the scale – it can search every available product, and curate a small selection of options to the human. Options which provide actual value.

- Commission Pressure: The AI becomes the new gatekeeper and can demand a significant share of the commission for driving a booking. The OTAs don’t have the previous ability to pay to get the top spots (yes, there will still be 2-3 paid spots, but not dozens). It’s only about value, not about trust and branding. One or two OTAs can survive here. Not 200.

- Shift from B2C to B2B: The opportunity that still exists for OTAs is to pivot from being a consumer-facing brand to being a data and inventory source for the AI. Their value becomes their robust APIs, global inventory, and booking infrastructure that the LLM can plug into. But there is also competition for that role. The AI agent needs only unique offers. An identical product option at $1 more than the next offer will never see the light of day.

2. Legacy Distributors (e.g. GDS)

Potential for a renaissance as the foundational plumbing of the new ecosystem.

The AI still needs structured, comprehensive data. It’s not efficient long-term for the AI to visit websites. There will be MCP servers (offering directories to suppliers) which the AI learns to trust. The nameservers of the AI world, which keep updated data for different sectors, saving the AI Agent the time and tokens to crawl them for each query..

- Hubs and Spokes for content: An AI cannot conversationally book a complex flight itinerary without access to the real-time, reliable data that a GDS provides. They are perfectly positioned to be the back-end data source for AI-powered travel agents.

- API Modernization: GDSs will face pressure to modernize their APIs to be more flexible and easily consumable by LLMs.

- Competitive Threat from Direct Connects: Their primary threat is the long-term trend of AI models finding direct API connections (also via the upcoming MCPs) with major travel brands, potentially bypassing the GDS, and other middlemen and their fees.

3. Suppliers

The ultimate opportunity for direct bookings at scale, but with a severe risk of brand commoditization.

This shift presents both the biggest opportunity and the biggest threat for suppliers.

- The Direct Booking Dream: AI could finally level the playing field against OTAs. If the AI determines a supplier’s direct booking channel offers the best value, then that’s who gets the booking. Saving the supplier those pesky commission fees.

- Brand Commoditization: The customer’s trust shifts from the brand to the AI (“My Assistant recommended this, which is all I need to know”). The supplier risks becoming a faceless, interchangeable commodity.

- Data is the key: Suppliers with poor digital infrastructure, sparse content, undiscoverable product information, limited photos, or outdated availability will become invisible to the AI. This is an area where the OTAs will stay ahead for the short to medium term.

4. Startups

Competing with the LLMs general travel discoverability will be futile. The opportunity lies in specialization and enabling technology (B2B).

- Hyper-Niche Agents: Startups can build specialized AI agents on top of foundational LLMs. It’s possible that these niche offerings could retain some eyeballs for the long term. Examples: “The world’s best AI planner for vegan travelers,” or “An AI that plans trips based on historical events.” These can provide depth where general models have breadth.

- Enabling Technology (Picks and Shovels): Huge opportunities will exist in building tools for the other players. Many distributors have moats around distribution (e.g. offline) which could remain immune to disruption. These players still need the AI tools to service their customers. Others with customer bases from outside of the industry (e.g. Financial institutions) also need similar tools to give them a way into the sector.

- New Discovery Platforms: Startups MIGHT be able to create AI-powered platforms that help travelers break away from the algorithm. Thanks to Meta and TikTok, the anti-algorithm movement may arrive, opening up space for new players to move in to.

5. LLMs (The AI Platform Providers)

Travel examples have been used in almost every major LLM announcement since the launch of ChatGPT. It’s a huge industry, and a very obvious place to attract new customers, offer them a great experience and keep them loyal to their flavor of AI.

- Monetization: The revenue potential from travel booking commissions is enormous. The LLM that provides the most trusted and seamless travel planning experience will earn a reliable revenue stream.

- Trust and Liability: This is their biggest challenge. If an AI books the wrong flight or recommends an unsafe hotel, who is liable? Establishing trust, accuracy, and a clear framework for handling errors is critical. This is where OTAs will still be able to thrive. It’s very possible the LLMs will allow a few points to the intermediary who provides this part of the service.

- The Data: The quality of an AI’s travel recommendations is directly proportional to the quality and comprehensiveness of its data. These companies are already light years ahead in terms of data. They may not have the previous travel booking data, but they have the up-to-date actual data that matters for humans making decisions.

6. Customers

The end-user experience will be transformed, with significant pros and cons.

- Simplicity: No more 57 browser tabs. Complex, multi-stop itineraries can be planned in a single, natural-language conversation.

- Hyper-Personalization: The AI will know your travel history, loyalty status, seating preferences, budget, style of travel etc – and with the multiple personas that the OTAs could never dream of understanding. It will plan trips that are truly tailored to you today, without the nonsense guesswork from previous OTA attempts at personalization.

- The Algorithm: It will be unclear why the AI recommended a specific option. As long as it performs, our trust will increase. Where it makes mistakes though, it will easily convince us that it wasn’t to blame.

The Filter Bubble & the Algorithm again: The AI may continuously recommend places and experiences similar to what you’ve done before. It’s very easy to break outside of this (just ask it) to discover new experiences, but most people won’t. Cruises and all-inclusive resorts will be safe for a little while longer, until the AI works out that variety is good for you, and it prioritizes your well-being ahead of your perception of free-will.

Who did I miss?

My guess: Google and OpenAI will become the first $10 Trillion companies, and will move towards a clean sweep here until somebody works it out and the regulators move in.