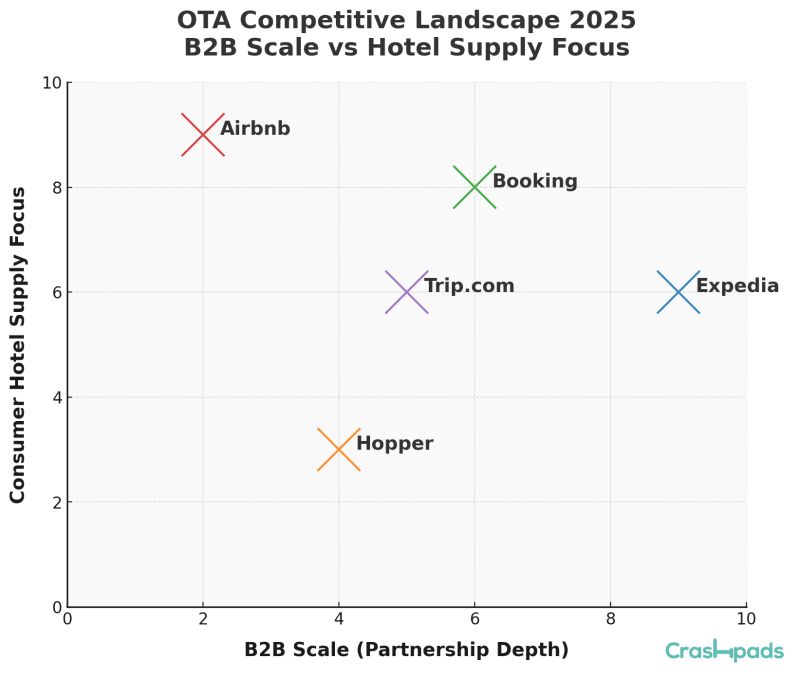

✈️ The Next Battleground in Online Travel: My Take

Dennis Schaal at Skift recently highlighted how Expedia, Booking, and Hopper are reshaping their strategies. What stood out to me wasn’t just the moves themselves, but the bigger picture of the real OTA battleground now shifting from consumer clicks focus to B2B distribution and for others new hotel supply.

My take on the Shifts:

*Expedia Group: The king of B2B with 70,000+ partners. Expanding APIs into cars, insurance, ads and leveraging its scale for a powerful flywheel of demand and supply. Probably the most stable and diversified OTA model today.

*Booking Holdings: Historically B2C-first, but finally plans consolidating Booking.com, Priceline, and Agoda into a single B2B division (2026). This is overdue, but with its global supply depth, this could be a game changer if executed well.

Hopper: The fintech newbie. By embedding travel into Capital One, Uber, and Air Canada with price freezes and disruption protection, Hopper proves that innovation, not size, can drive sticky partnerships and resonates with youth.

Airbnb: The wildcard challenger. Targeting independent hotels first for higher ROI and more willing partners compared to chains (Marriott, Hilton, Wyndham). Add in strategic hires they have made to lead partner efforts, supply team investments, and the tech foundation laid with Experiences, and Airbnb looks set up to deliver a “complete trip” ecosystem more seamlessly than the old guard.

📊 Margins for the Models

B2B – Lower volatility, longer contracts, predictable revenue (Expedia’s B2B margins are already double its B2C margins).

B2C – Higher margin but potential, subject to Google’s distribution tax and seasonal volatility.

Airbnb – Sacrificing near-term margin to secure independent hotels and optimize for future high-ROI supply growth.

My Takeaway

The OTA of the future won’t just be the one that wins consumer clicks. It will be the one that best balances:

B2B reach thru scale + distribution

Hotel supply especially from independents (higher margins), and

Fintech & tech innovation (stickier, “complete trip” experiences).

Right now:

Expedia owns B2B scale

Airbnb is rewriting the supply playbook

Booking is reorganizing to catch up

Hopper is innovating on the edges.

And let’s not forget Trip.com Group dominant in Asia, owner of Skyscanner, but still trailing in global B2B innovation.