Highlights

- Calendar shifts flattened hotel performance

- Growth continues in hurricane-affected markets

- Group demand returned, exceeding 2019 levels

- Double-digit global RevPAR gains, again

- Taylor Swift arrived in Canada

Two negative calendar shifts, one positive

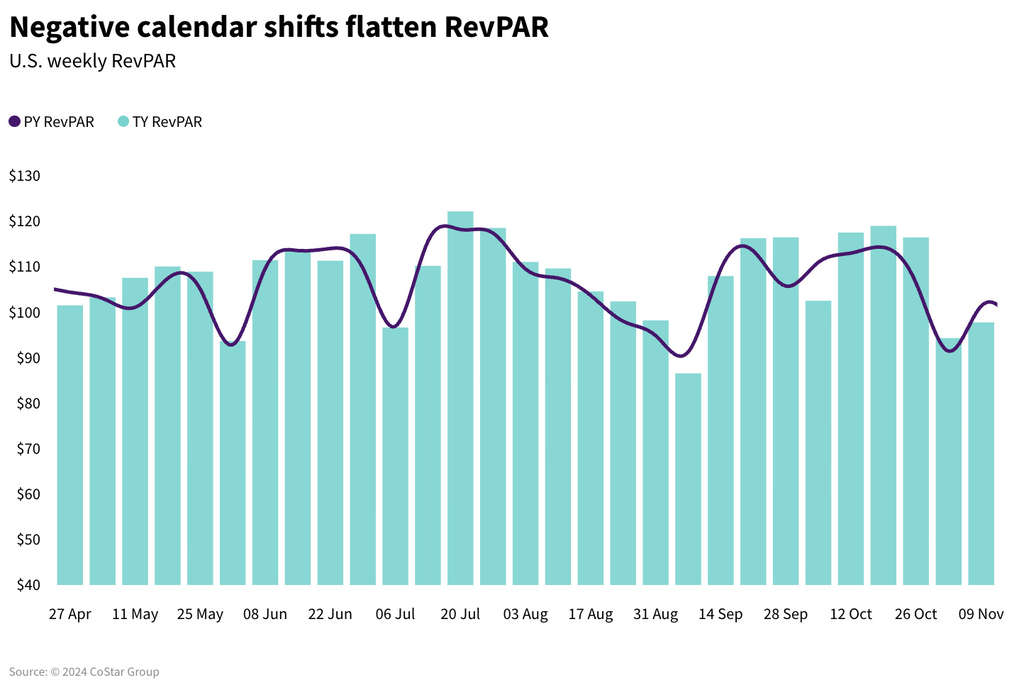

The week was expected to be strong, but calendar shifts slowed U.S. hotel performance and created almost flat revenue per available room (RevPAR) for the week ending 16 November 2024 (+0.4%). Occupancy increased 0.9 percentage points (ppts), while average daily rate (ADR) declined 1.1%. Three notable calendar shifts occurred – two negative and one positive.

- The Formula 1 Grand Prix race in Las Vegas was held one week earlier last year on 16-18 November. The 2024 event is 21-23 November. Recall, Las Vegas represents 2.9% of U.S. room supply, and when significant events occur in that market, the impact is felt in the national averages. Recalculating overall U.S hotel performance without Las Vegas, RevPAR rose 4.3%, mostly on ADR. Occupancy increased at the same rate (0.9ppts) as the total industry.

- Veteran’s Day 2024 fell on Monday this year versus a Friday in 2023 and, more importantly, it was a week later. As a result, Monday’s RevPAR dropped 5.3% versus 2023.

- Thanksgiving is a week later this year, meaning demand did not drop in this most recent week as it did during the 2023 comparable. As a result, RevPAR Tuesday through Thursday was up, with Wednesday posting the largest gain at 5.1%. The weekend, however, was depressed with RevPAR retreating 2.2%, the result of falling ADR (-3.5%) and occupancy (-0.9ppts).

The impact of the above shifts was magnified across the Top 25 Markets. While RevPAR was flat for the industry, the measure decreased 3% in the Top 25 Markets, entirely due to falling ADR (-5.2%). Las Vegas as mentioned was down significantly. Excluding that market, RevPAR in the Top 25 Markets increased 4.8%. Regardless of including or excluding Las Vegas, RevPAR on Monday (Veteran’s Day) was down (-8.6% with, -7.7% without). However, RevPAR from Tuesday to Thursday was +6.6% without Las Vegas versus -0.1% with it. Weekend (Friday & Saturday) RevPAR was also dramatically different falling 3% on ADR versus rising 4.8% without Vegas.

Markets and chain scales boosted across the country

Across the Top 25 Markets, Tampa, New Orleans, Houston, and San Diego experienced RevPAR increases over 20% as these markets all reported strong group demand. Tampa also saw sustaining gains amid Hurricane Milton rebuilding. In addition to Tampa, other markets affected by Hurricane Helene and Hurricane Milton continued to see solid demand growth. Over the past four weeks, seven markets (Augusta, Columbia, Florida Central South, Greenville/Spartanburg, North Carolina West, Sarasota and Tampa) have seen double-digit occupancy increases each week netting RevPAR gains from 20%-30%. In the most recent week, hotels in those markets saw RevPAR grow 34% via occupancy (+15.2ppts) and ADR (+8.6%). Hotels in all chain scales in these markets saw double-digit RevPAR gains, however, the impact was most pronounced among Midscale and Economy hotels, which saw RevPAR gains of 82.8%. Upscale/Upper Midscale hotels increased RevPAR 32.9%, while Luxury/Upper Upscale hotels increased 11.7%.

Sports once again left a mark on the weekend across many parts of the country with the following markets scoring 50% weekend RevPAR gains: Pittsburgh (Urban-Bennett Basketball Invitational and Pitt Panthers football), Georgia North (Georgia Bulldogs), Madison (Wisconsin Badgers), and Louisville (North American Championship Rodeo).

All chain scales increased RevPAR, bookended by Luxury (+5.7%) and Economy (+3.6%). Occupancy gains drove the top three chain scales while ADR gains were more dominant across the lower three. In a similar pattern, the top three chain scales experienced the largest RevPAR gains in markets outside the Top 25 while the bottom three chains scales experienced the most growth in the Top 25 Markets.

Group demand returned

Group demand among Luxury and Upper Upscale hotels rebounded and exceeded the level seen in 2019, a year when Thanksgiving was also a week later, meaning this week is comparable to 2019. Group demand increased 1.8% to 2.1 million rooms, ~20,000 rooms more than in 2019. ADR declined 3.4% due entirely to Las Vegas. Excluding Vegas, group ADR was up 3.6%. Transient demand increased a robust 4.3% while transient ADR declined 4.7%. Excluding Las Vegas had minimal impact on transient performance.

Global growth sprint continues

Global RevPAR, excluding the U.S., advanced 10.2%. That was the third consecutive week of double-digit growth, driven primarily by ADR (+7.7%), as occupancy increased less than two percentage points to 70.3%. RevPAR was strongest at the beginning of the week with Sunday up 17.5%. The next three days remained in double-digits until Thursday when RevPAR was still up a robust 9.4%. Weekend RevPAR was similar to what was seen on Thursday (+9.0% and +7.4%, respectively). ADR was the main driver of RevPAR gains after Sunday.

For a second consecutive week, Japan led the top countries in RevPAR growth (+22.9%) with ADR again the primary driver as occupancy was soft. Mexico was the second strongest performer with a significant RevPAR lift in Mexico City (+44.5%) and Baja California (+48.6%). Indonesia and Italy reported double-digit growth with most markets across each country reporting gains. Canada also increased by double digits with the country benefitting from the first weekend of Taylor Swift’s Eras Tour in Toronto, with ADR over the concert days (Thursday – Saturday) increasing120.4% to $388 USD while occupancy dropped 1.1 ppts to 76.0%.

Final Thoughts

RevPAR is expected to be strong in the week ending 23 November 2024 via a final business/conference travel sprint ahead of Thanksgiving. STR’s Forward STAR data clearly shows strong occupancy gains given the easy comparable to last year, which contained Thanksgiving. Plus, the Formula 1 Grand Prix race will also provide a bounce in ADR, but not as much as last year based on what we have heard from hoteliers in the market. Of course, it’s all relative as many hotels in that market will see ADR that is up to five times higher than the average hotel in the industry. The week of Thanksgiving (week ending 30 November 2024) itself will be slow. The December holiday season will be compressed because of the late Thanksgiving, which should generally produce positive performance.

Canada will continue to receive a boost from Taylor Swift’s tour with one more weekend in Toronto followed by Vancouver, ending her welcomed contribution to the hotel industry and global economy. Top global countries are expected to continue seeing strong yet slowing RevPAR growth.

*Analysis by Isaac Collazo, Chris Klauda.

About CoStar Group, Inc.

CoStar Group (NASDAQ: CSGP) is a leading provider of online real estate marketplaces, information, and analytics in the property markets. Founded in 1987, CoStar Group conducts expansive, ongoing research to produce and maintain the largest and most comprehensive database of real estate information. CoStar is the global leader in commercial real estate information, analytics, and news, enabling clients to analyze, interpret and gain unmatched insight on property values, market conditions and availabilities. Apartments.com is the leading online marketplace for renters seeking great apartment homes, providing property managers and owners a proven platform for marketing their properties. LoopNet is the most heavily trafficked online commercial real estate marketplace with thirteen million average monthly global unique visitors. STR provides premium data benchmarking, analytics, and marketplace insights for the global hospitality industry. Ten-X offers a leading platform for conducting commercial real estate online auctions and negotiated bids. Homes.com is the fastest growing online residential marketplace that connects agents, buyers, and sellers. OnTheMarket is a leading residential property portal in the United Kingdom. BureauxLocaux is one of the largest specialized property portals for buying and leasing commercial real estate in France. Business Immo is France’s leading commercial real estate news service. Thomas Daily is Germany’s largest online data pool in the real estate industry. Belbex is the premier source of commercial space available to let and for sale in Spain. CoStar Group’s websites attracted over 163 million average monthly unique visitors in the third quarter of 2024. Headquartered in Washington, DC, CoStar Group maintains offices throughout the U.S., Europe, Canada, and Asia. From time to time, we plan to utilize our corporate website, CoStarGroup.com, as a channel of distribution for material company information. For more information, visit CoStarGroup.com.

This news release includes “forward-looking statements” including, without limitation, statements regarding CoStar’s expectations or beliefs regarding the future. These statements are based upon current beliefs and are subject to many risks and uncertainties that could cause actual results to differ materially from these statements. The following factors, among others, could cause or contribute to such differences: the risk that future media events will not sustain an increase in future occupancy rates. More information about potential factors that could cause results to differ materially from those anticipated in the forward-looking statements include, but are not limited to, those stated in CoStar’s filings from time to time with the Securities and Exchange Commission, including in CoStar’s Annual Report on Form 10-K for the year ended December 31, 2023 and Forms 10-Q for the quarterly periods ended March 31, 2024, June 30, 2024, and September 30, 2023, each of which is filed with the SEC, including in the “Risk Factors” section of those filings, as well as CoStar’s other filings with the SEC available at the SEC’s website (www.sec.gov). All forward-looking statements are based on information available to CoStar on the date hereof, and CoStar assumes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.