A new study from McKinsey & Company highlights a shift that goes beyond retail. While European consumers remain cautious about spending, their behavior is changing rapidly, especially in how they research and plan travel. The findings come from the March 2026 ConsumerWise survey, authored by Jessica Moulton and Pavlos Exarchos, and focus on consumer sentiment across France, Germany, Italy, Spain, and the United Kingdom.

At first glance, the macro picture looks familiar. Consumers across Europe entered 2026 with a cautious outlook. Confidence remains mixed, with inflation still the dominant concern and geopolitical tensions increasingly influencing sentiment. France, in particular, showed the highest levels of pessimism, even if slightly improved compared to late 2025.

But beneath that stable surface, behavior is shifting quickly, and this is where travel and hospitality players should pay close attention.

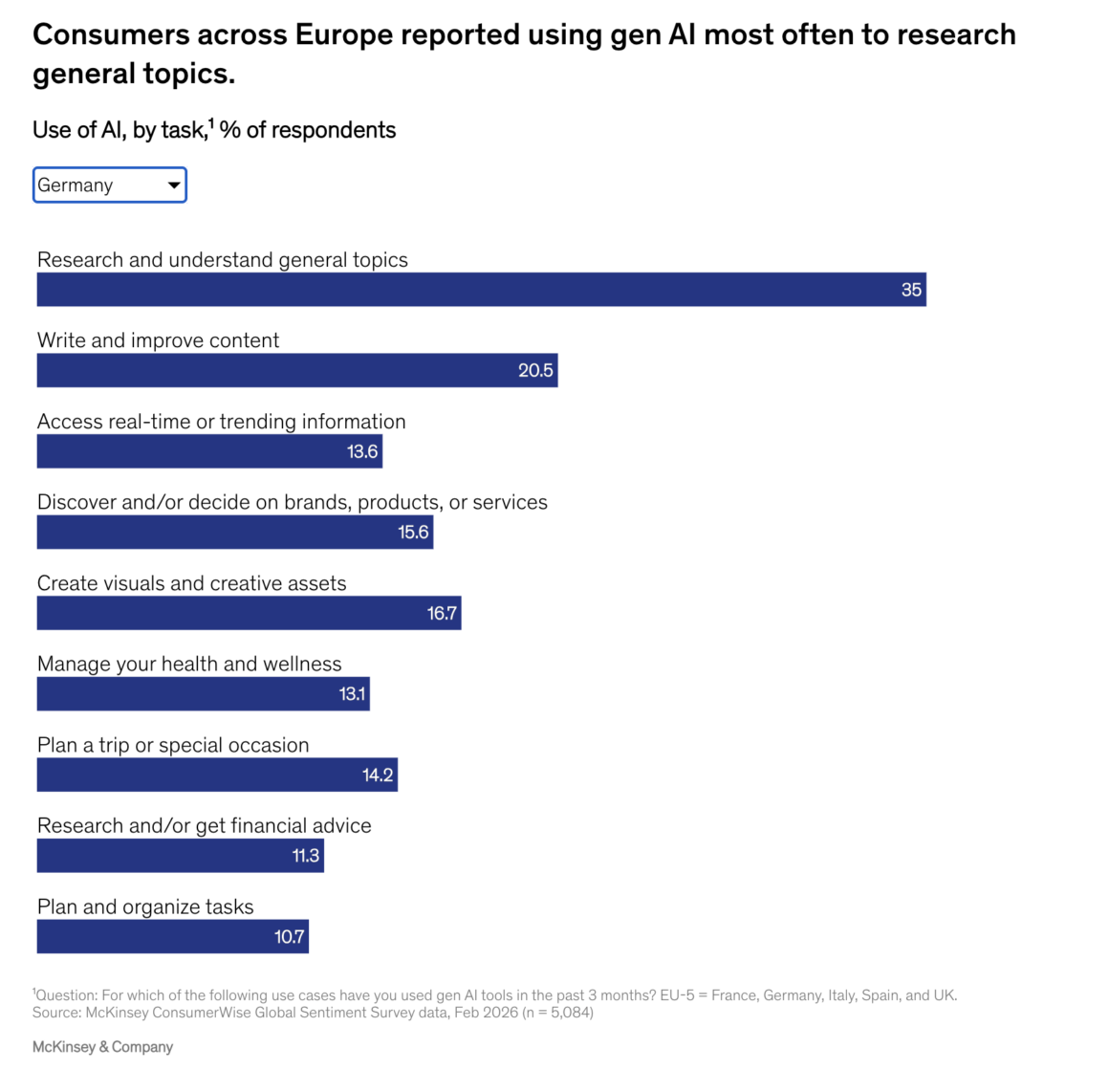

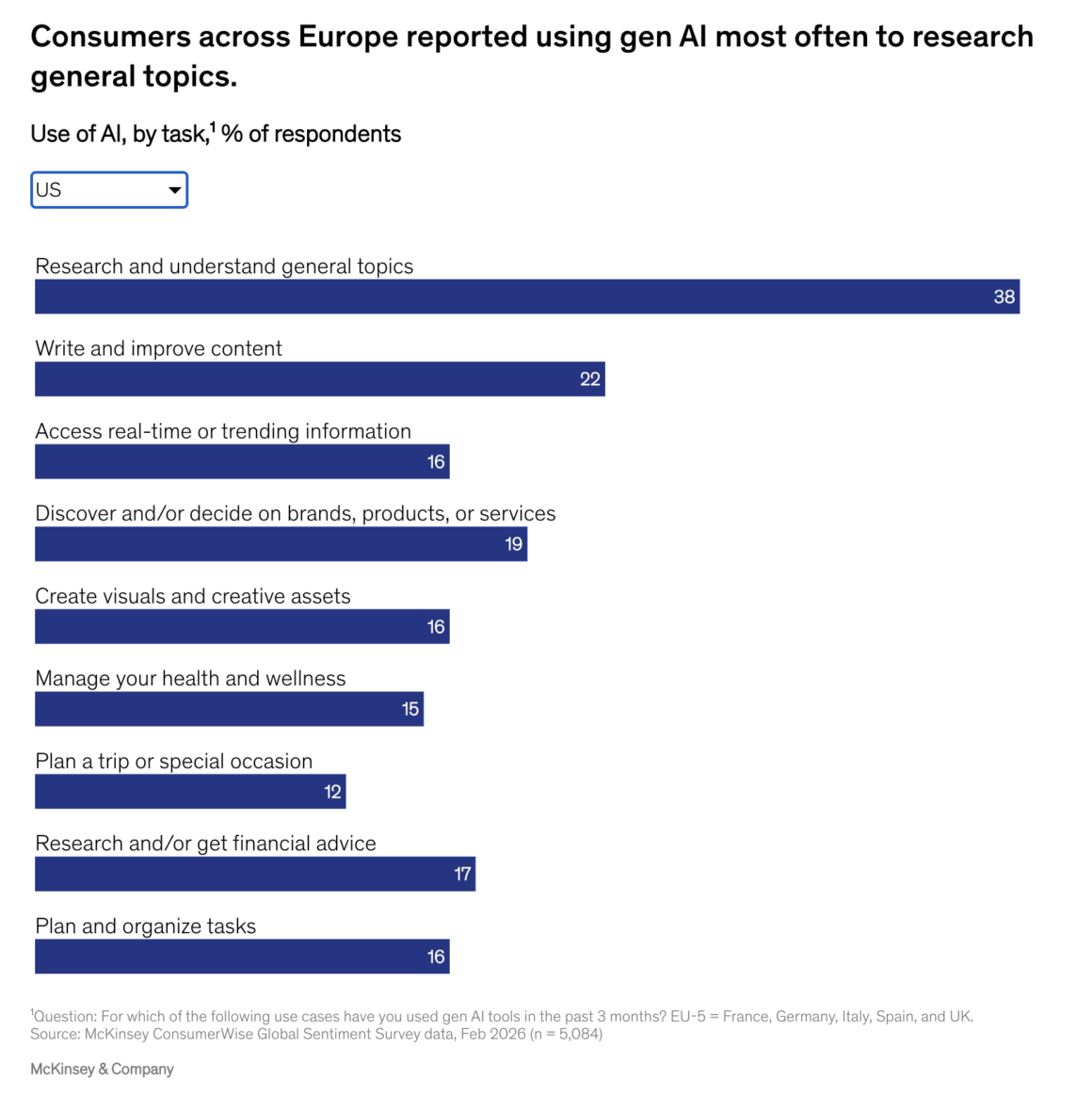

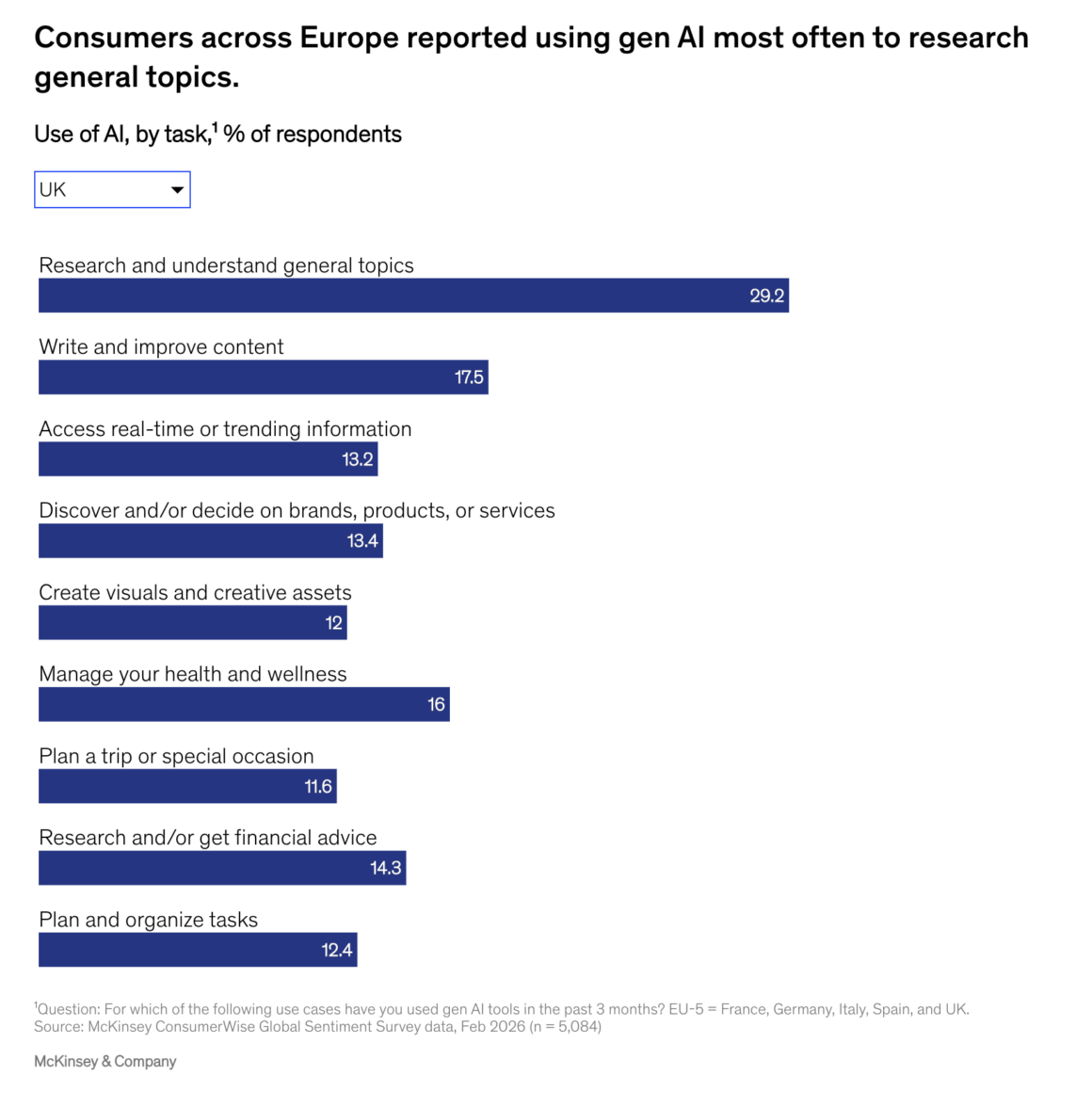

One of the most striking findings is the rapid adoption of generative AI tools. Across the EU-5, between 59 percent and 74 percent of consumers reported using AI in the past three months. France sits at 63 percent, while Italy leads at nearly 74 percent. This alone signals a structural change in how consumers approach decision-making.

More importantly for the hotel industry, travel stands out as a leading use case. European consumers are now more likely than their US counterparts to use AI tools specifically for planning trips or special occasions. This is a critical signal. AI is not just influencing what people buy, but where they go, how they compare destinations, and ultimately which hotels make it into consideration.

However, AI is not yet replacing the booking journey. McKinsey’s data shows that consumers primarily use these tools for early-stage decision-making. Roughly half of users rely on AI to learn about destinations, discover brands, or get inspiration. Around 40 percent use it to compare options. Fewer than a quarter use it for transactions such as booking or post-purchase support.

This suggests a clear shift. AI is becoming the new top of the funnel.

For hotels, this has direct implications. Visibility is no longer just about OTAs or search rankings. It increasingly depends on how well a property, brand, or destination is understood and surfaced by AI systems during the research phase. If a hotel is not part of that discovery layer, it may never even enter the consideration set.

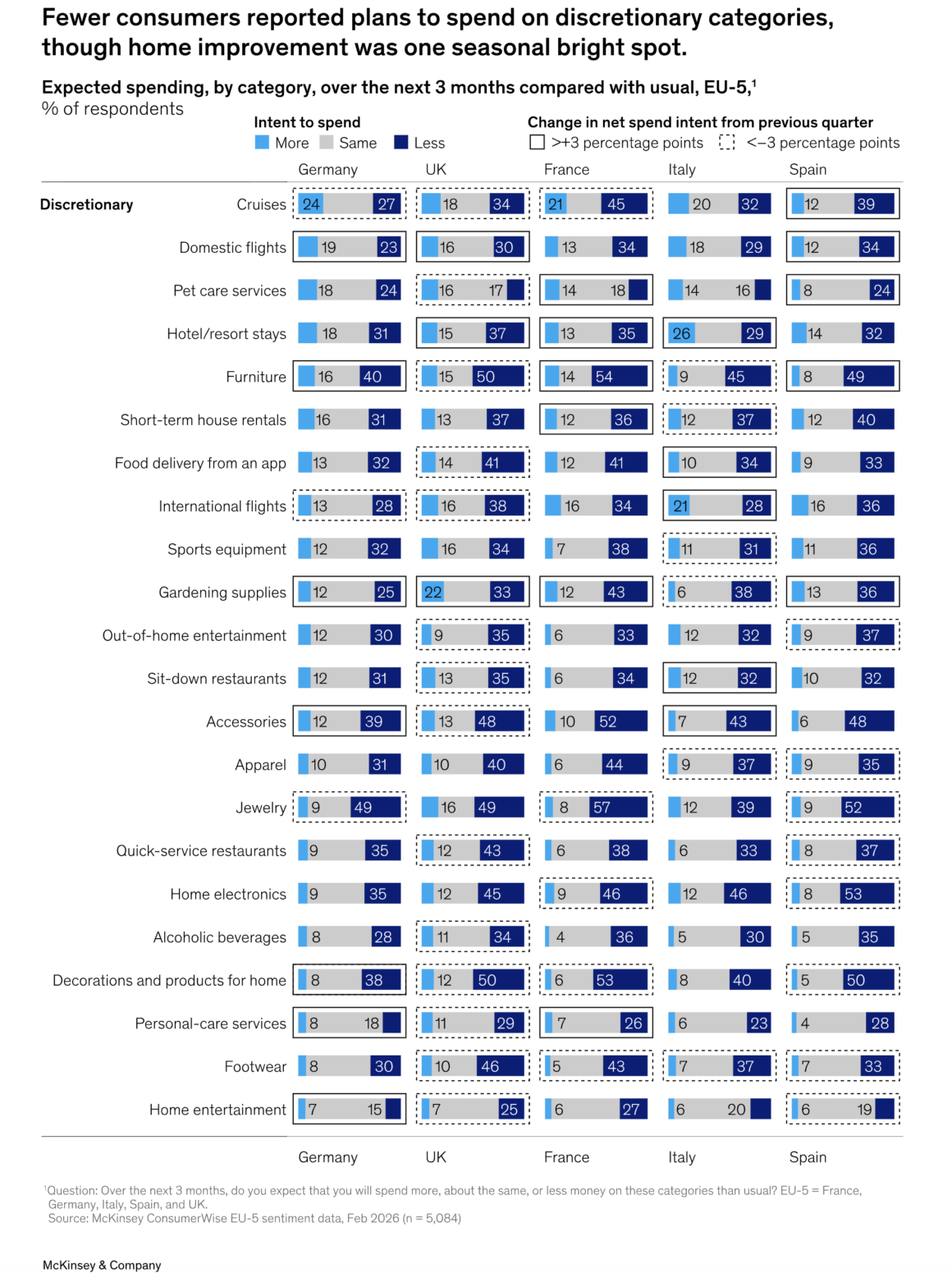

At the same time, spending intent in travel remains uneven. McKinsey reports mixed signals across categories. Fewer Europeans plan to spend on cruises in the coming months, while intentions around flights and hotel stays vary significantly by country. In Germany, for example, demand for domestic flights and hotel stays is increasing, while international travel is softening.

This fragmentation reinforces a key point. There is no single European traveler profile in 2026. Demand is becoming more localized, more situational, and more sensitive to economic context.

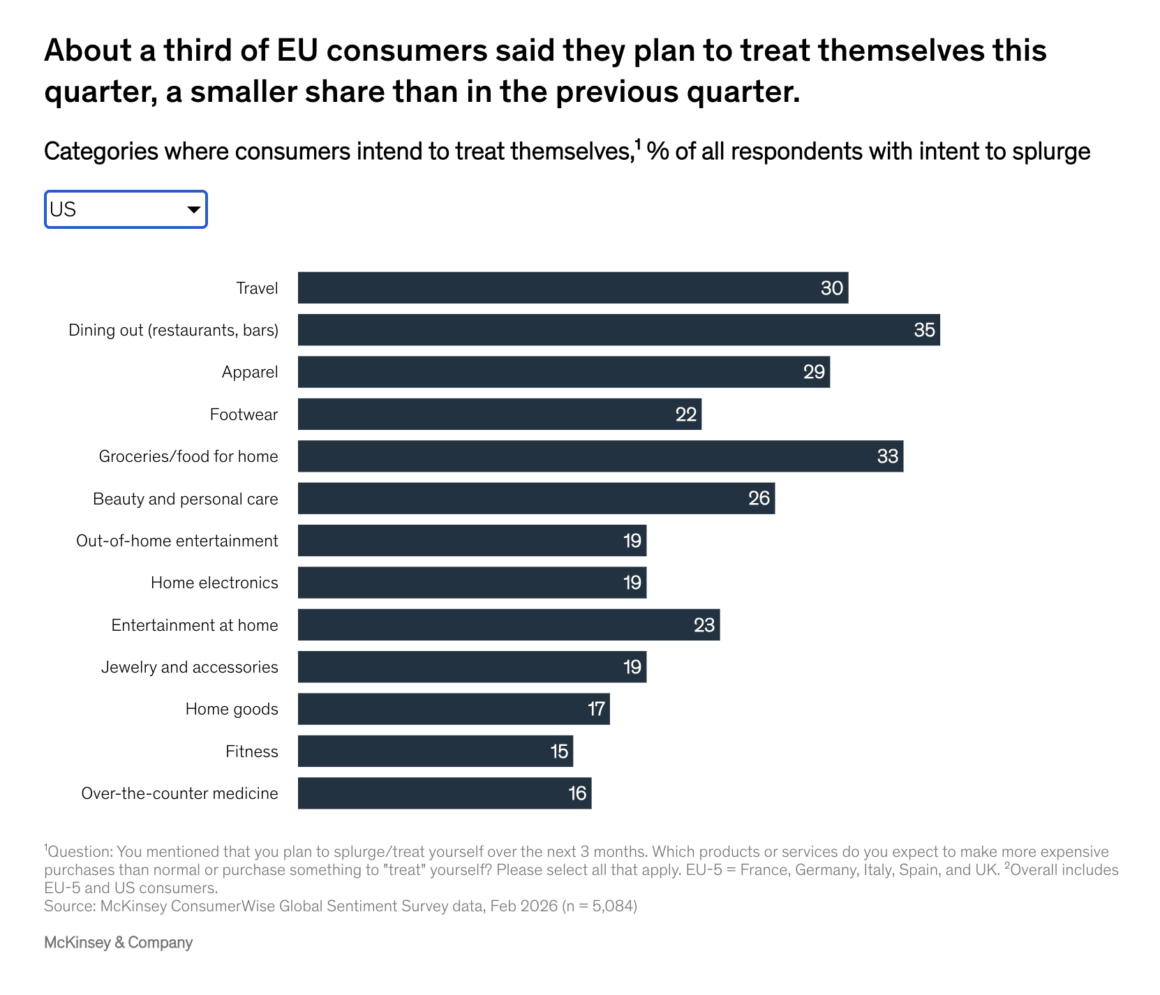

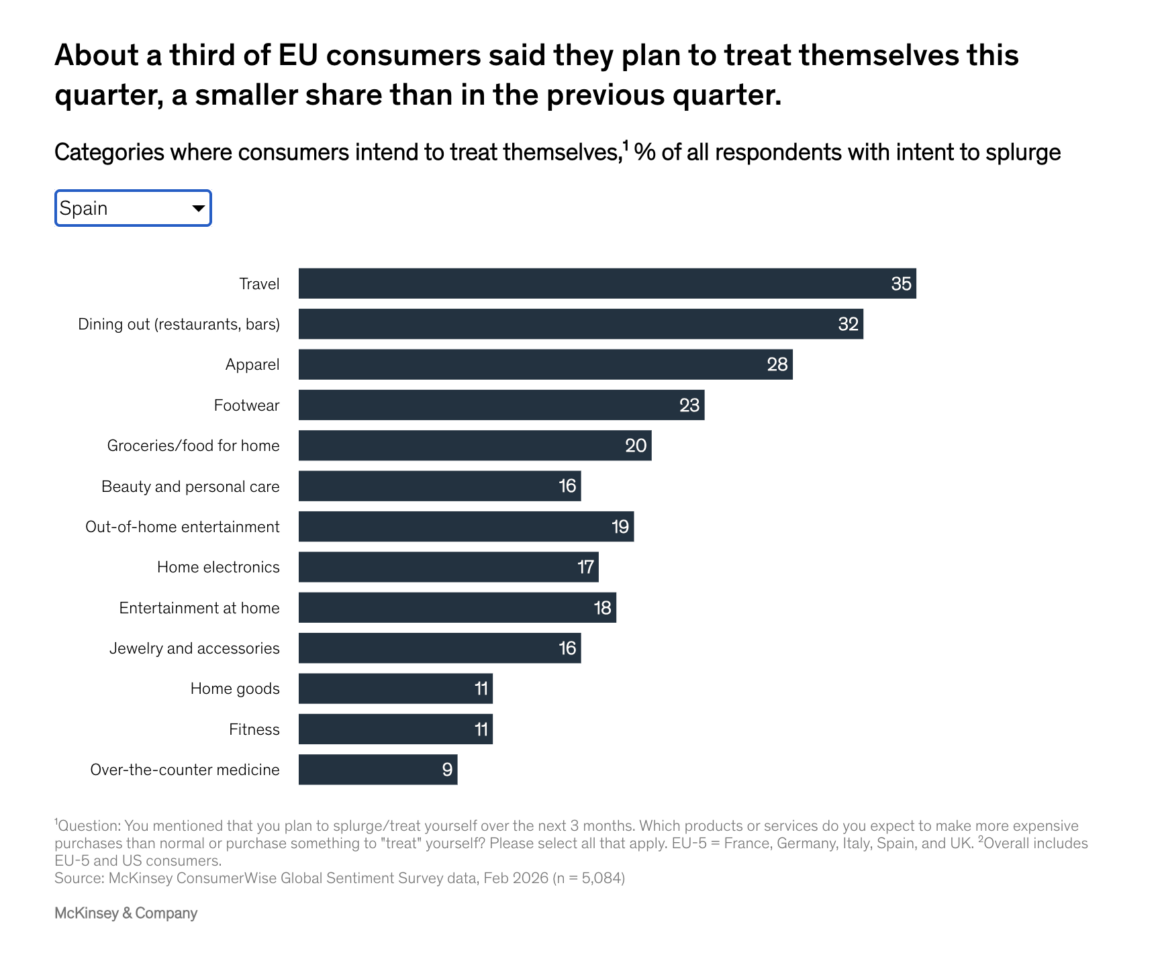

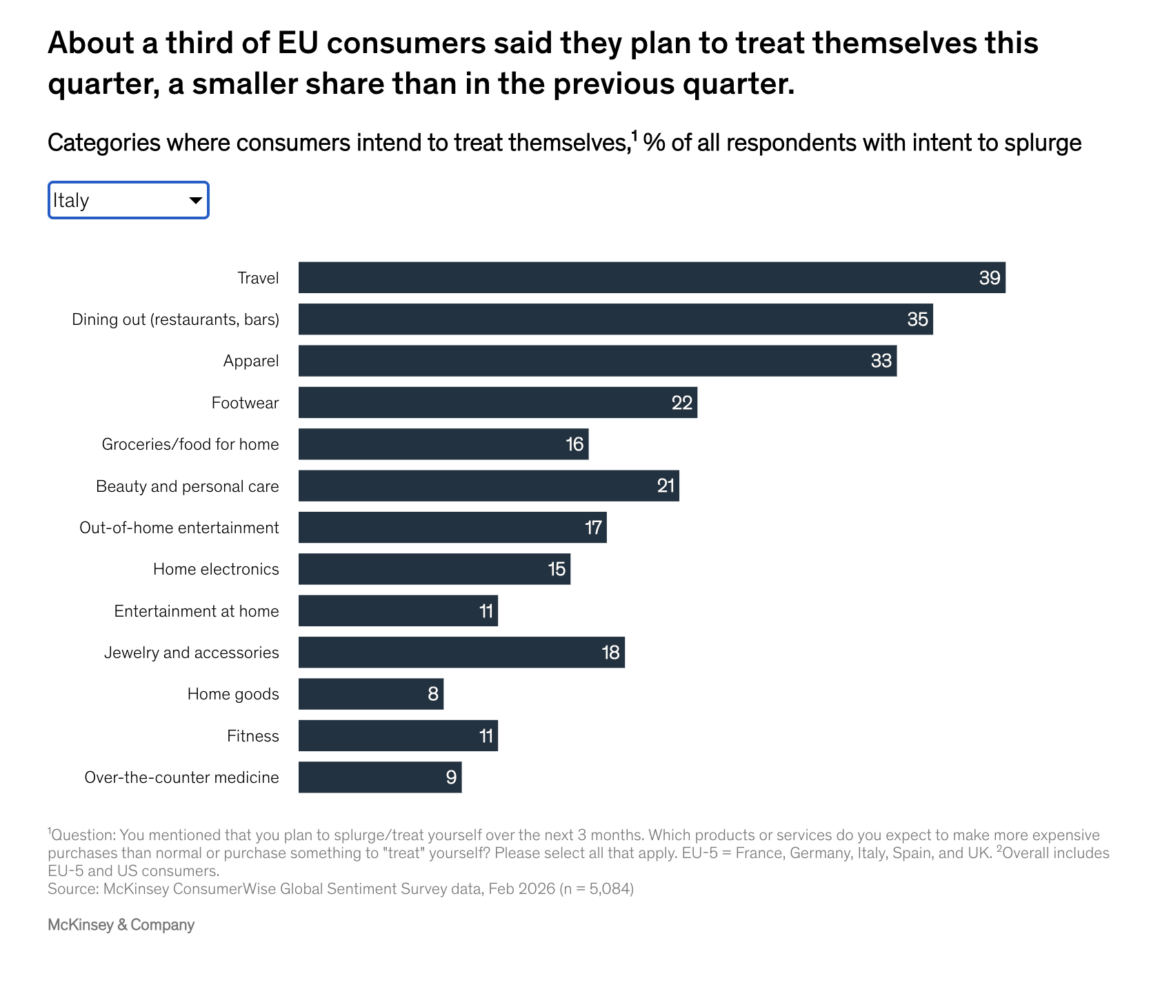

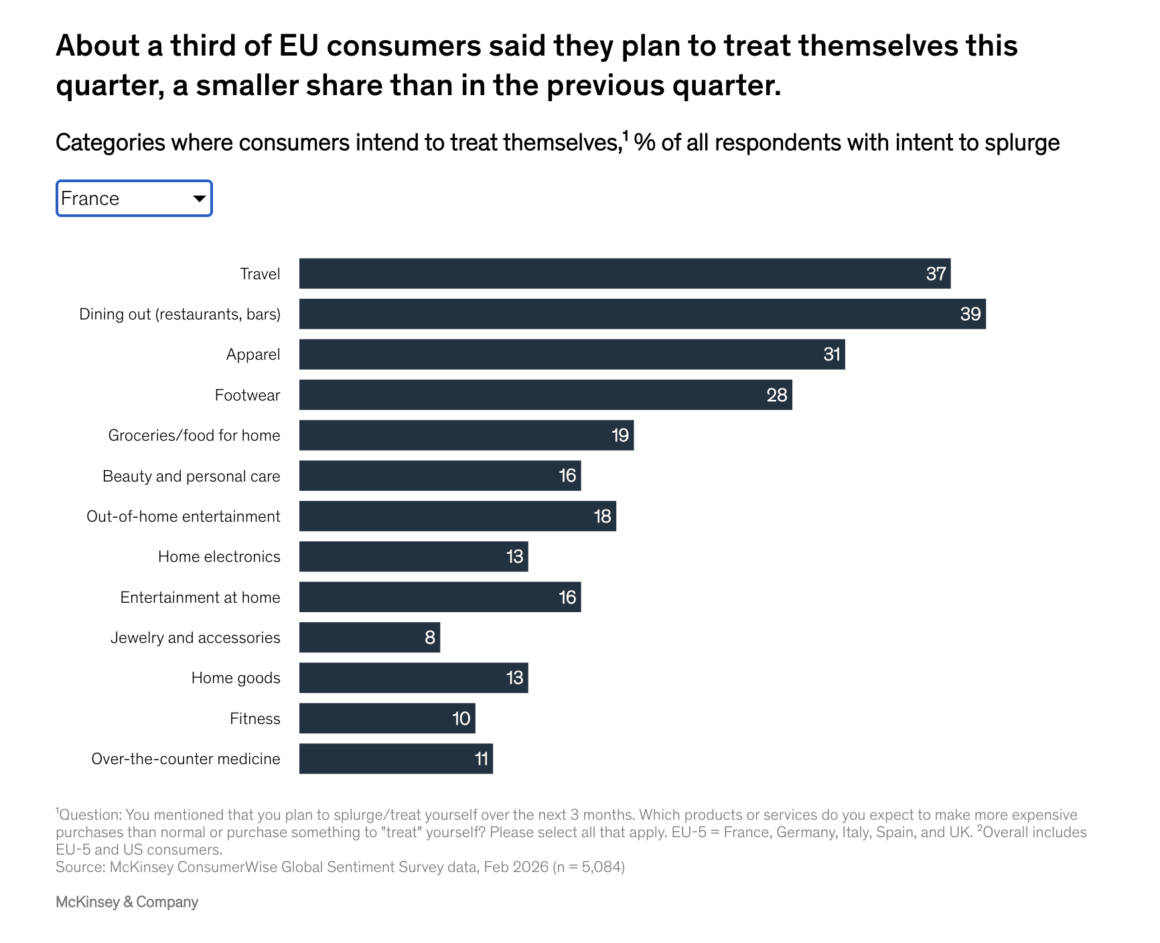

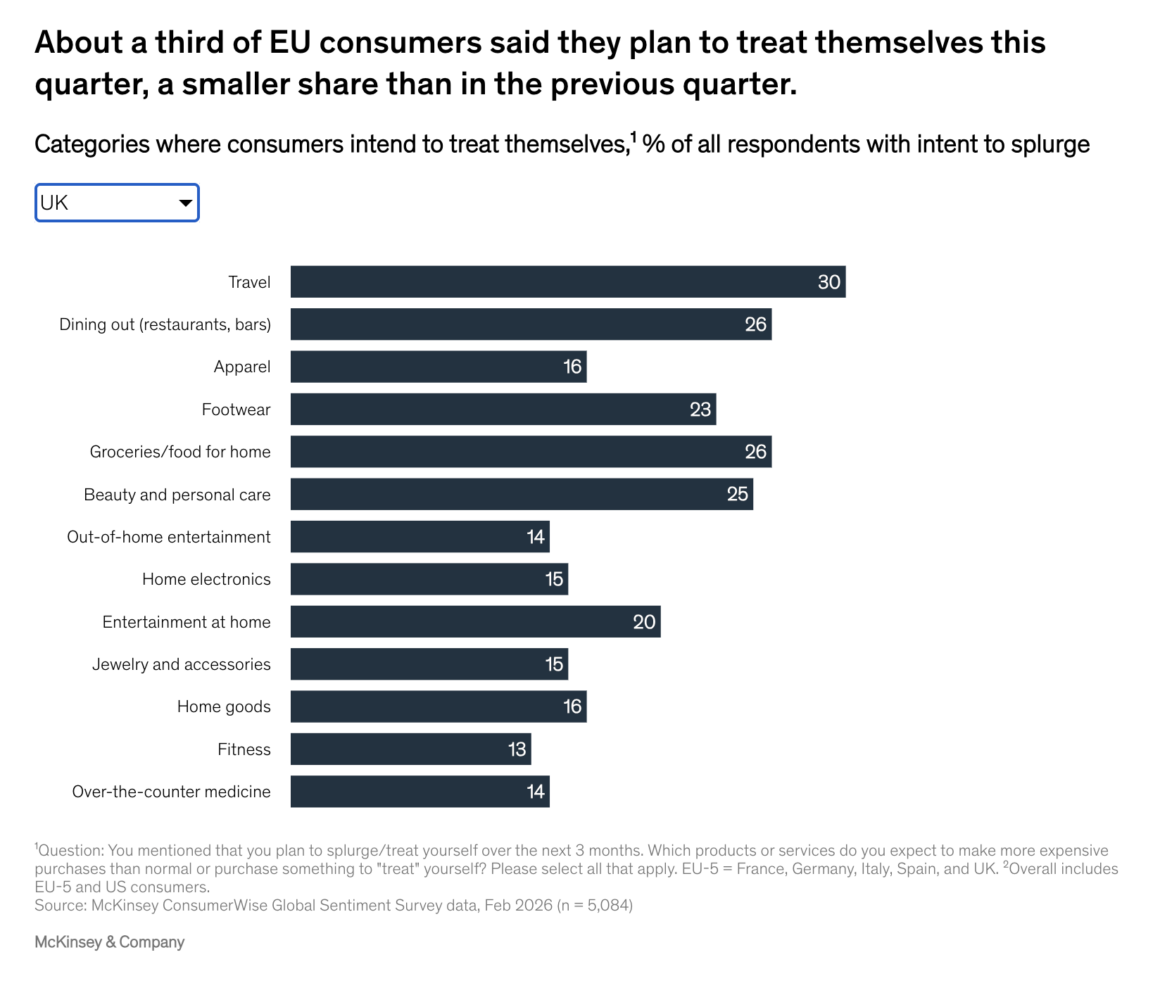

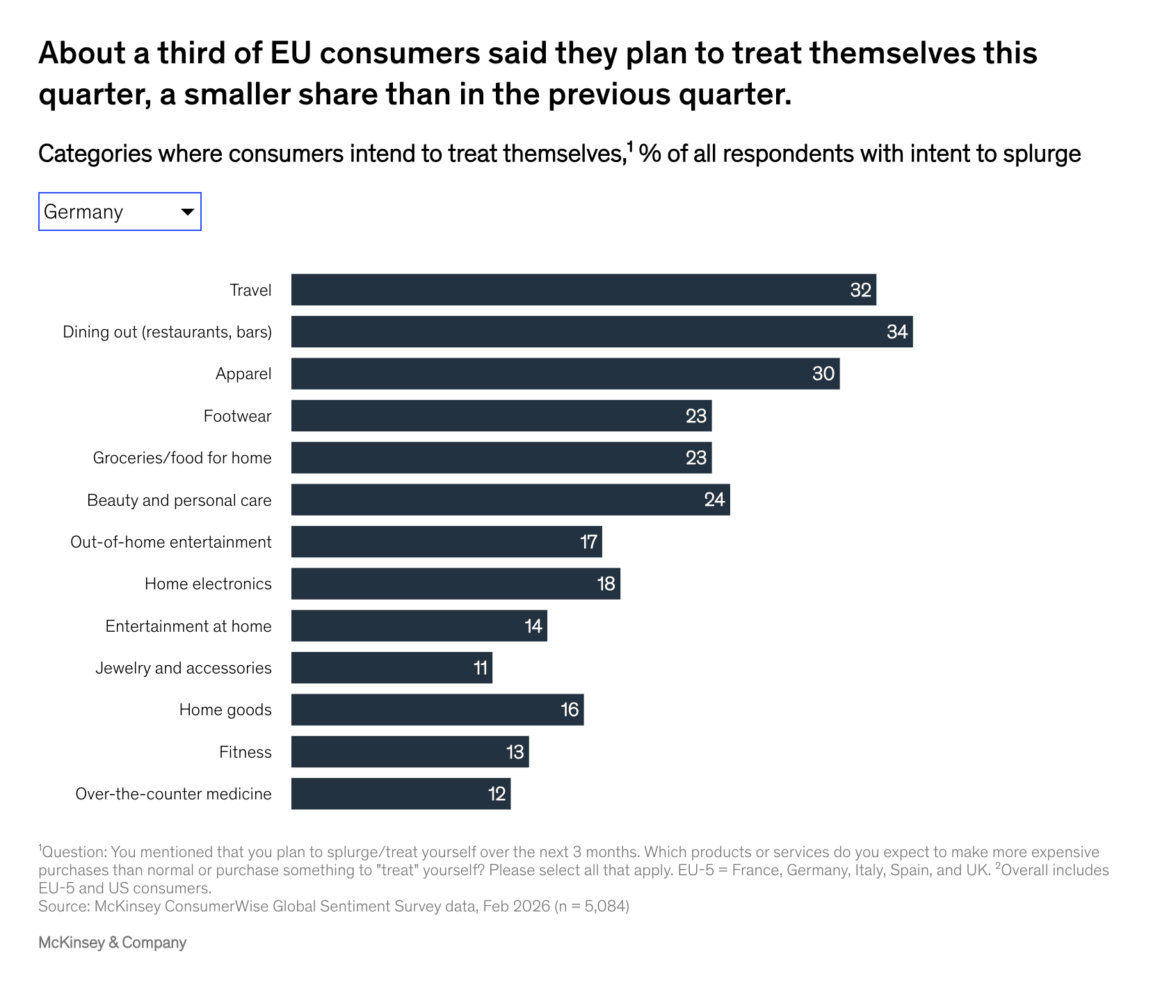

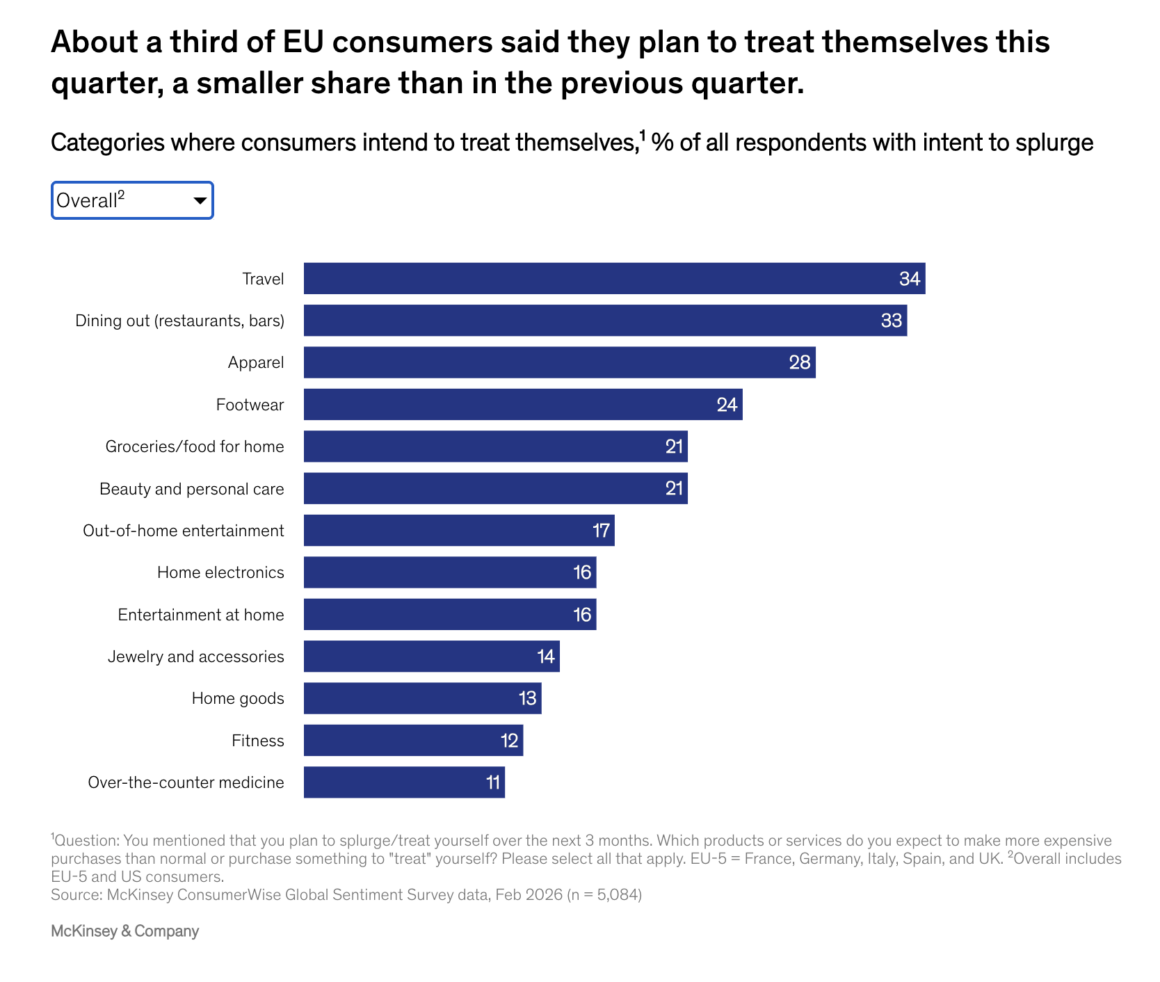

Another important signal is the decline in discretionary spending. Only about one third of European consumers say they plan to “treat themselves” this quarter, down five percentage points compared to late 2025. This tightening directly affects higher-end and impulse-driven travel segments.

Taken together, the message for hospitality operators is clear. Consumers are still traveling, but they are more selective, more value-driven, and increasingly guided by AI in how they choose.

The opportunity lies in adapting to this new discovery layer. Hotels that understand how AI tools interpret, compare, and recommend options will have a significant advantage. Those that rely solely on traditional channels risk becoming invisible at the very moment decisions are being shaped.

As McKinsey concludes, consumers in Europe are not spending freely, but they are becoming more digital, more informed, and more deliberate. In travel, that shift may redefine how demand is captured long before a booking is ever made.