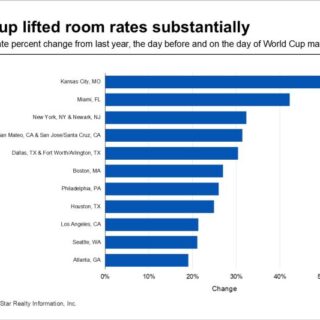

Philadelphia Leads U.S. Hotel Market Growth with 19.6% ADR and 32.1% RevPAR Increase in Late July 2026

🏨 Philadelphia and St. Louis hotels saw notable performance gains from July 26 to August 1, 2026. Philadelphia's ADR rose 19.6% to $175.02 and RevPAR increased 32.1% to $137.55, aided by Morgan Wallen concerts. St. Louis experienced a 15.1% occupancy lift, ADR grew 13.5% to $140.98, and RevPAR rose 30.6% to $106.27. Las Vegas faced declines with occupancy at 66.2% (-11.7%), ADR at $145.87 (-6.2%), and RevPAR at $96.63 (-17.1%). CoStar's data encompasses 95,000 properties globally.

Share