This article is a recap of a recent LinkedIn post by hospitality entrepreneur and industry commentator Bashar Wali. We are republishing the key takeaways here and encourage readers to view the original post for the full context and discussion (and charts).

According to Bashar Wali, hoteliers and investors attending this year’s NYU International Hospitality Investment Forum may have heard dozens of presentations, but the industry’s outlook can largely be distilled into three key realities: an acquisition window driven by constrained supply, a widening divide between luxury and economy performance, and unrealistic expectations surrounding the 2026 FIFA World Cup.

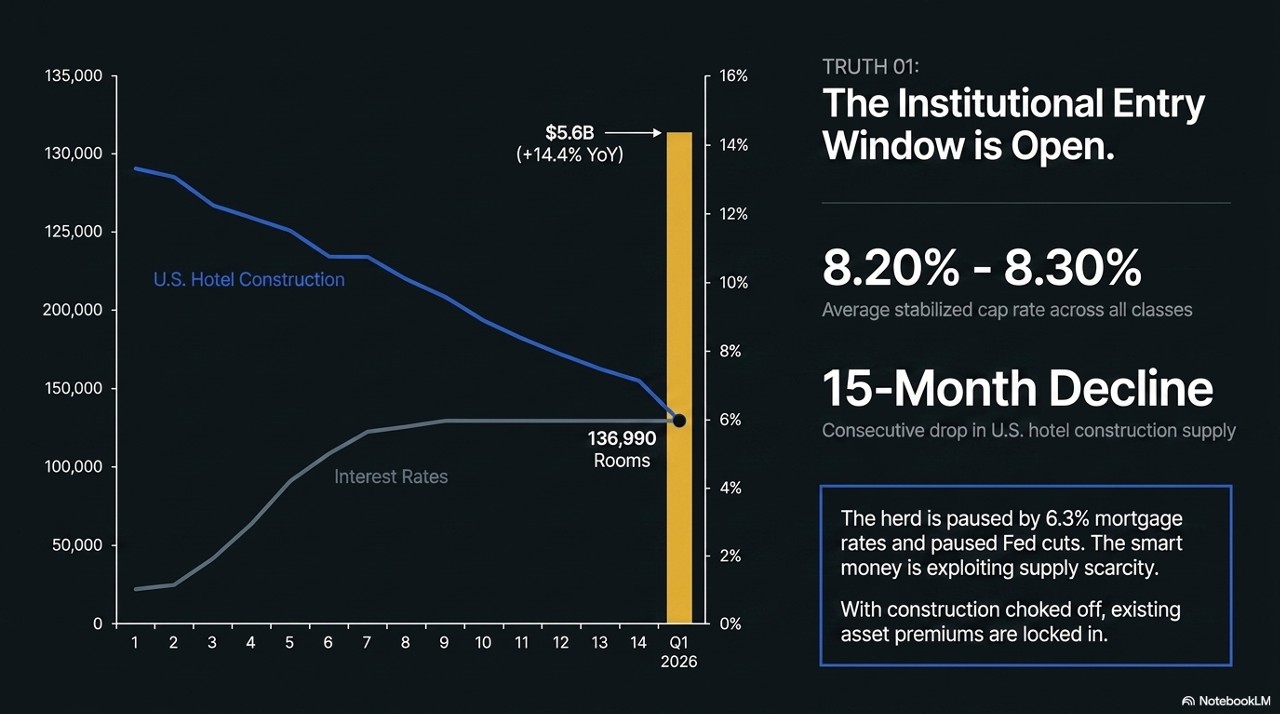

The first theme is what Wali describes as an institutional entry window. New hotel development in the United States continues to slow as elevated financing costs limit construction activity. The presentation highlights a 15 month decline in hotel construction supply, with approximately 136,990 rooms currently in the pipeline and stabilized cap rates averaging between 8.2% and 8.3% across the market.

The implication is straightforward. With fewer new hotels entering the market, existing assets become more valuable. Investors willing to deploy capital today may benefit from supply scarcity over the coming years, particularly if interest rates begin to ease while new construction remains constrained.

The second takeaway focuses on what Wali calls the “K-shaped consumer.” Rather than viewing the hotel industry through national averages, he argues that performance is increasingly split between market segments.

Luxury and upper upscale hotels continue to outperform. The presentation cites first quarter 2026 RevPAR growth of 7.8%, supported by resilient high income travelers who remain willing to absorb higher room rates. Operators in this segment are encouraged to maximize pricing power and drive ancillary revenue through experiences, food and beverage, and other guest spending opportunities.

At the other end of the spectrum, economy and midscale hotels face a much tougher environment. RevPAR declined by 2.1% during the same period, while operators face increasing pressure on margins. In these segments, the focus shifts toward cost control, labor efficiency, and protecting profitability rather than chasing rate growth.

The broader lesson is that averages can be misleading. Performance depends heavily on customer segment, location, and positioning. A rising market for luxury hotels does not automatically translate into success for the broader industry.

The final point challenges one of the biggest narratives currently circulating in North America: the anticipated impact of the 2026 FIFA World Cup.

According to Wali, many hoteliers are overestimating demand based on large room blocks reserved by FIFA and related organizations. As those blocks expire and unused inventory returns to the market, some host cities could experience a sharp correction in expectations. He refers to this as the “phantom demand shock.”

His advice is to focus less on occupancy forecasts and more on rate strategy. Historical booking patterns suggest that a significant share of World Cup demand materializes within 30 days of match dates. Blanket restrictions and aggressive blackout policies may ultimately limit opportunities rather than maximize them.

Taken together, Wali’s message is that the hospitality industry is entering a period where nuance matters more than headlines. Supply constraints are creating opportunities for investors, consumer spending patterns are becoming increasingly polarized, and major events may not deliver the demand surge many operators expect. The winners will be those who look beyond industry averages and focus on the realities of their specific market.

You can read Bashar Wali’s original LinkedIn post for the complete presentation and supporting data.